📣 Create Blog for Traders!

Stop Watching news - Start Making it.

START

War Risk Resets Global Markets as Gold and the Dollar Lead

The joint US-Israeli strike targeting Iran’s leadership has abruptly repriced global geopolitical risk. In a matter of hours, the market shifted into a full war-risk regime, reshaping cross-asset behaviour in ways that could define the rest of 2026.

In this environment, conventional defensive frameworks are proving unreliable. Below, Ultima Markets outlines a practical war-time allocation lens—highlighting where capital is finding real shelter and where hidden vulnerabilities remain.

This episode is defined by a rare combination: rising inflation expectations alongside heightened geopolitical stress. That mix is rewriting traditional correlations.

Gold and the US Dollar Lead

Gold has reasserted itself as the primary store of value, surging beyond $5,400 per ounce and approaching historic territory.

At the same time, the US Dollar Index has staged a decisive rebound, retracing February’s losses. The simultaneous long Gold and long USD positioning has become the dominant institutional flight-to-safety allocation.

The Bond Market Breakdown

What stands out most is the failure of US Treasuries to provide traditional protection.

Although the 10-year note initially rallied, it quickly reversed as inflation expectations climbed. Instead of absorbing risk, long-duration bonds amplified volatility.

- Stagflation Pressure: European natural gas prices spiked more than 30 percent in a single session, reigniting global inflation concerns.

- Yield Repricing: Yields across US, UK, and German sovereign debt are rising rather than falling, reflecting stagflation risk rather than deflationary fear.

- Conclusion: Long-duration government bonds are currently behaving as a volatility source, not a stabiliser.

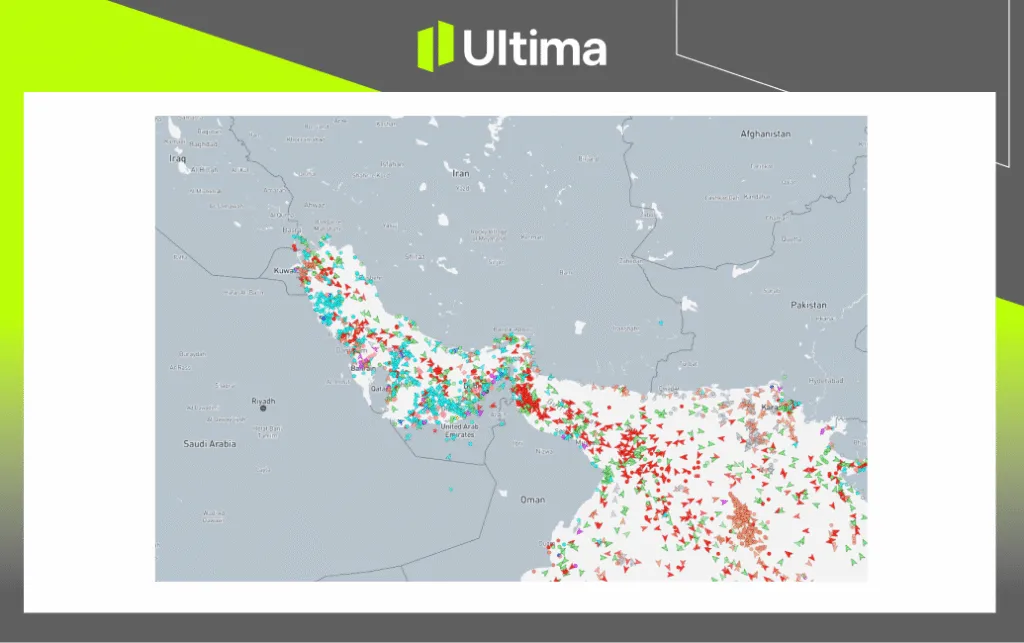

Before seeking opportunity, investors must quantify tail risk. The focal point of this crisis is the Strait of Hormuz, through which a significant portion of global energy supply transits.

With the IRGC declaring a blockade and reports of tanker disruptions emerging, the crude market sits at a structural inflection point.

Scenario A: Limited Disruption (Base Case)

If the situation remains contained or is resolved quickly:

- Supply Cushion: OPEC+ retains more than 2.8 million barrels per day of spare capacity and has already signalled production increases.

- Price Outlook: WTI likely stabilises below $80, with resistance concentrated in the $74 to $77 range.

Under this outcome, risk premium moderates rather than explodes.

Scenario B: Full Blockade (Tail Risk)

A complete halt of regional exports would trigger a supply shock with severe consequences. In such a case, crude could accelerate toward $100, with extreme scenarios implying localised spikes far beyond that level.

Strategic Assessment

Available intelligence indicates targeted airstrikes weakened Iranian naval capacity. There is no confirmed evidence of maritime mining operations, which would signal prolonged disruption.

At present, the situation resembles an ambiguous, headline-driven blockade rather than a fully enforced physical shutdown.

Given the binary nature of the energy risk, allocation discipline is essential.

Focus on Structural Safe Havens

- Gold: Continues to function as the primary geopolitical hedge. In early conflict phases, the path of least resistance typically remains upward.

- US Dollar: Despite testing technical resistance near the 200-day moving average, the macro environment favours USD strength.

In a widening conflict scenario, forced deleveraging across asset classes could trigger a liquidity scramble. In that setting, USD liquidity outperforms.

Central Bank Constraints

Rising energy costs complicate monetary policy.

The ECB and BOE may need to temper rate-cut expectations in response to renewed inflation risk, effectively tightening financial conditions.

Investors should not rely on rapid central bank accommodation. The inflation impulse of conflict limits policy flexibility.

Selective Opportunity After Dislocation

While sentiment is fragile, structural demand drivers for certain assets remain intact.

Watchlist Themes:

- Copper, as a proxy for industrial demand

- AUD, reflecting commodity linkage

- Japanese and South Korean equities, tied to resilient export and manufacturing bases

The approach is measured accumulation during volatility rather than reactive chasing. Gap closures and panic-driven discounts can present tactical entry points.

Summary

Avoid reflexively chasing crude higher. The geopolitical premium is elevated, and volatility remains extreme.

In the current phase, capital preservation revolves around Gold and USD liquidity. More cyclical exposures—such as Copper or select Asian equities—should be approached opportunistically once the immediate headline shock subsides and price structure stabilises.

This is no longer a standard risk cycle. It is a regime shift, and portfolio construction must adjust accordingly.

Navigating and trading the forex markets requires clarity, discipline, and access to reliable insights. Ultima Markets is committed to providing data-driven analysis to support informed trading decisions.

Join Ultima Markets today and stay connected with us by following us on social media for the latest news, events, and product updates. Visit UM Academy and access unlimited educational trading resources to help you master the markets.

—–

Trading leveraged derivative products carries a high level of risk and may not be suitable for all investors. Leverage can magnify both gains and losses, potentially resulting in rapid and substantial capital loss. Before trading, carefully assess your investment objectives, level of experience, and risk tolerance. If you are uncertain, seek advice from a licensed financial adviser. Leveraged products are not intended for inexperienced investors who do not fully understand the risks or who are unable to bear the possibility of significant losses.

Comments, news, research, analysis, price, and all information contained in the article only serve as general information for readers and do not suggest any advice. Ultima Markets has taken reasonable measures to provide up-to-date information, but cannot guarantee accuracy, and may modify without notice. Ultima Markets will not be responsible for any loss incurred due to the application of the information provided.