📣 Create Blog for Traders!

Stop Watching news - Start Making it.

START

Fertilizer Prices Are a Trap, Not a Buy Signal for 2026

Everyone expects agricultural prices to follow fertilizer costs higher. I think they're walking straight into a margin-crushing trap that will blow up accounts.

This morning, I was reviewing my spreadsheet of failed prop firm challenges—yeah, I still keep it. Failure #4, from back in 2021, stared back at me. The trade was simple: Oil futures were ripping, so I went long Canadian Dollar (CAD). The correlation was textbook. And it blew my account in three days as USD/CAD squeezed higher against all logic. It taught me a brutal lesson: obvious correlations are often the most dangerous trades. And looking at the chatter today about fertilizer prices, I'm seeing the exact same trap being set.

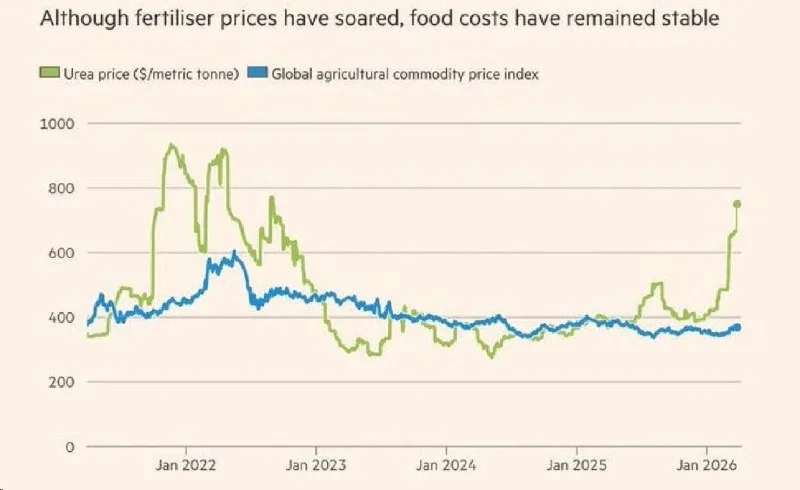

The news is out: fertilizer prices are surging, but agricultural product prices like corn ($ZC) and soybeans ($ZS) are stagnant. The consensus view, the 'easy trade,' is that ag prices will catch up after a multi-month lag. Buy the dip on grains and wait. It sounds logical. Input costs rise, so output prices must follow. But from my experience, the market rarely gives you a free lunch, and this feels like one of those trades designed to punish the crowd.

I'm calling foul on this one. This isn't a simple lag; it's the crack of a bullwhip. The surge in input costs is going to slash farmer margins to the bone. Before they can even think about passing those costs to consumers, they'll be forced to cut spending elsewhere. That's where the real trade is. The market isn't pricing in a simple delay; it's underestimating a full-blown margin collapse for the entire agricultural sector.

The historical link between fertilizer and crop prices is breaking down because of overwhelming macro headwinds. Farmers can't just raise prices if global consumers can't pay. Unlike past cycles, we're facing a potential global slowdown, a stubbornly strong dollar, and the ever-present threat of government intervention to control food inflation.

- Demand Destruction: As Emma Blackwood has pointed out about consumer sentiment, people are cutting back. High food prices won't stick if wallets are empty. Farmers can't sell what people can't afford.

- Strong US Dollar: A strong dollar makes US exports of corn and wheat more expensive for foreign buyers, creating a major headwind for prices, regardless of how much fertilizer costs.

- Government Intervention: Don't underestimate the political will to control food inflation. Price caps or subsidies could completely sever the link between input costs and final prices, leaving farmers holding the bag.

So if I'm not buying corn, what am I doing? I'm looking at the second-order effects. Who gets hurt first when farmers stop making money? The companies that sell them expensive equipment. I'm building a short position in Deere & Company ($DE). When a farmer's profits get vaporized by a 40% jump in fertilizer costs, the last thing they're doing is buying a new $500,000 combine.

This is the kind of setup I look for now. It's a core part of my FTMO challenge strategy for 2026. Instead of betting on a crowded, lagging indicator, I'm betting against the companies whose earnings will get hit first. The risk is clearly defined. I know Viktor Reyes has some compelling arguments for a commodity supercycle, and while I respect his calls on energy, the demand picture for agriculture feels much weaker to me. This isn't a resource scarcity play; it's a margin compression play.

I'm not jumping in blindly. I'm watching for a break of the $390 support level on $DE. My entry would be around $388, with a stop-loss just above the recent highs at $415. My first target is the $350 zone, a key support area from last year. This provides a roughly 2.5:1 risk/reward ratio, the kind of asymmetry you need to pass prop firm challenges. This is one of the key prop firm challenge tips and tricks: find trades where the potential reward is multiples of your risk.

My thesis is invalidated if we see a major government bailout or subsidy program for US farmers that directly offsets fertilizer costs. A sudden, sharp decline in the US Dollar would also make me reconsider, as it would boost the export market and could give farmers the pricing power they currently lack.

The market isn't pricing in a lag; it's pricing in a margin collapse. The easy trade is almost never the right one.

This is a classic case of the market focusing on a simple A-to-B relationship while ignoring the wider context. I failed enough challenges chasing those simple ideas. Now, I look for the stress points. The question isn't *when* crop prices will catch up to fertilizer. The real question is, what breaks first?