📣 Create Blog for Traders!

Stop Watching news - Start Making it.

START

Private Credit Stocks Plunge: A 2008 Echo or a Buy?

The market is panicking over private credit, selling off top-tier asset managers. My analysis shows this is a classic overreaction and I'm getting my buy list ready.

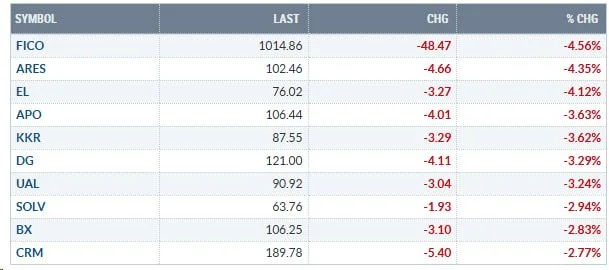

So here's what nobody seems to be talking about with the private credit sell-off today. Yes, the headlines are ugly. Seeing names like Blackstone (BX) down 8% and Ares (ARES) getting hit for a staggering 11% intraday is enough to make anyone nervous. The narrative is that the high-rate environment is finally cracking the foundation of the private markets. But from my desk, this looks less like a systemic collapse and more like a long-overdue reality check, creating the first real opportunity in this space in years.

Let's be clear: the pain is real. For two years, we've had sustained rates above 5%, and the chickens are coming home to roost for weaker, over-leveraged companies that took on floating-rate debt. This isn't a surprise; it's gravity. What we're seeing today is a reaction to whispers of a few large, syndicated private loans to mid-market tech and consumer discretionary companies showing serious signs of stress. The market is extrapolating this to mean the entire $1.7 trillion private credit market is about to implode.

This is where a macro overlay is critical. The pressure on these portfolio companies is immense. Think about the input cost inflation that Jake Morrison has been flagging with his analysis on crude oil. When energy and transport costs rise, it directly squeezes the margins of the exact companies these funds lend to, making it harder to service that debt. It's all connected. The market sells first and asks questions later, and right now, it's selling everything with the words 'private credit' attached to it.

No, this is not a repeat of 2008. The current private credit market differs fundamentally from the subprime mortgage crisis. The leverage is primarily held by sophisticated institutional investors—pensions, endowments, and sovereign wealth funds—not retail banks. This creates a more stable, albeit illiquid, capital base that is less prone to a bank-run panic.

The key difference is in the structure and the lenders. In '08, the risk was opaque, wrapped in complex derivatives (CDOs), and deeply integrated into the global banking system. Today, these are direct loans. While there will be defaults—and my models are pricing in a default cycle uptick to 4-5% from the historical 1-2%—it's an earnings and valuation problem for the fund managers, not a systemic solvency crisis for the financial system.

When I see a sector-wide sell-off, my first instinct is to hunt for the best-in-class operators being unfairly punished. I spent the morning digging back into the 10-K filings for Blackstone and Ares. The market is pricing these companies based on their performance fees (carried interest), which will certainly take a hit. But it's ignoring their massive, sticky fee-related earnings (FRE) from management fees. For BX, FRE covers their dividend and then some. That's the floor.

This is where I start looking for some of the best value stocks undervalued by this panic. My focus narrows to firms with strong fundraising momentum and a higher allocation to senior-secured, first-lien debt, which offers more protection in a downturn. This is a flight to quality.

- Blackstone (BX): The behemoth. Diversified across credit, real estate, and PE. I'm adding to my long-term position if it breaks below $110. My DCF model suggests fair value is closer to $145 in a normalized environment.

- Ares Management (ARES): A more pure-play credit manager. Their direct lending platform is arguably the best. The 11% drop today is a severe overreaction. I'm a buyer starting at $115 with a target of $150 over 18 months.

- Blue Owl Capital (OWL): A name people often overlook. They specialize in lending to the upper mid-market and have a strong permanent capital base. Watching this one closely for an entry below $16.

My bullishness is predicated on this being a contained, albeit painful, repricing of risk, not the start of a deep recession. If the upcoming earnings season preview Q1 2026 shows a dramatic slowdown in corporate spending and guidance, I'll have to reassess. A sharp spike in unemployment above 5.5% would be the ultimate invalidation signal, as that would trigger a cascade of defaults far beyond what even the bears are currently pricing in.

This is also where the broader market picture matters. A geopolitical event, the kind of thing Alex Volkov watches closely, could easily tip the scales. Given this new credit stress, my overall S&P 500 price target 2026 is now more cautious; I'm pulling it back from 6,000 to a more conservative 5,850 until we see how this plays out.

The market is selling the entire private credit sector on a narrative, but the fundamentals of the best-in-class managers tell a different story. This is a stock-picker's market now.

Ultimately, I'm a buyer of quality into this weakness. I've seen these panics before, and they almost always punish the good with the bad. The question I keep asking myself is this: is the market correctly pricing in a 2008-level credit event, or is this the best buying opportunity in alternative asset managers we've seen in the last five years?